Unlock the full potential of your business with commercial financing solutions. A well-structured business credit line provides access to necessary funds, allowing you to navigate fluctuating cash flows and capitalize on growth opportunities. By understanding the various capital solutions available, you can make informed decisions to propel your business forward, whether it’s managing day-to-day expenses or investing in long-term expansion strategies. Discover the benefits of business credit lines and how they can be tailored to meet the unique needs of your growing enterprise, helping you stay ahead in today’s competitive market. Effective financial management starts here.

Commercial financing is a crucial aspect of growing a business, and it’s essential to understand the various capital solutions available to entrepreneurs. In this guide, we will explore the world of commercial financing, focusing on business credit lines and their benefits.

Understanding Commercial Financing

Commercial financing refers to the process of obtaining funds or capital to support the growth and development of a business. This can include loans, lines of credit, and other forms of financing. It’s essential to understand the different types of commercial financing available, as each has its own set of terms and conditions.

Types of Commercial Financing

There are several types of commercial financing options available to businesses, including term loans, lines of credit, and invoice financing. Each type of financing has its own advantages and disadvantages, and it’s crucial to choose the right option for your business needs. The following table provides an overview of the different types of commercial financing:

| Type of Financing | Description |

|---|---|

| Term Loan | A loan with a fixed interest rate and repayment term |

| Line of Credit | A revolving credit facility that allows businesses to borrow and repay funds as needed |

| Invoice Financing | A type of financing that allows businesses to borrow against outstanding invoices |

Benefits of Business Credit Lines

Business credit lines offer several benefits to entrepreneurs, including access to funds when needed, flexibility in repayment, and increased cash flow. With a business credit line, you can borrow and repay funds as needed, making it an ideal solution for businesses with seasonal fluctuations or unpredictable cash flow. The interest rates on business credit lines are often lower than those on other types of financing, making it a cost-effective solution.

How to Qualify for a Business Credit Line

To qualify for a business credit line, you’ll need to meet certain eligibility criteria, including a good credit score, stable cash flow, and a solid business plan. The lender will also consider your business history, industry, and growth potential when determining your eligibility. It’s essential to prepare a strong application and provide detailed financial information to increase your chances of approval.

Best Practices for Managing a Business Credit Line

To get the most out of your business credit line, it’s essential to manage it effectively. This includes monitoring your credit limit, making timely payments, and avoiding overspending. You should also review your credit agreement carefully and understand the terms and conditions of your credit line. By following these best practices, you can maximize the benefits of your business credit line and grow your business with confidence. Strong financial management and strategic planning are key to making the most of your commercial financing options.

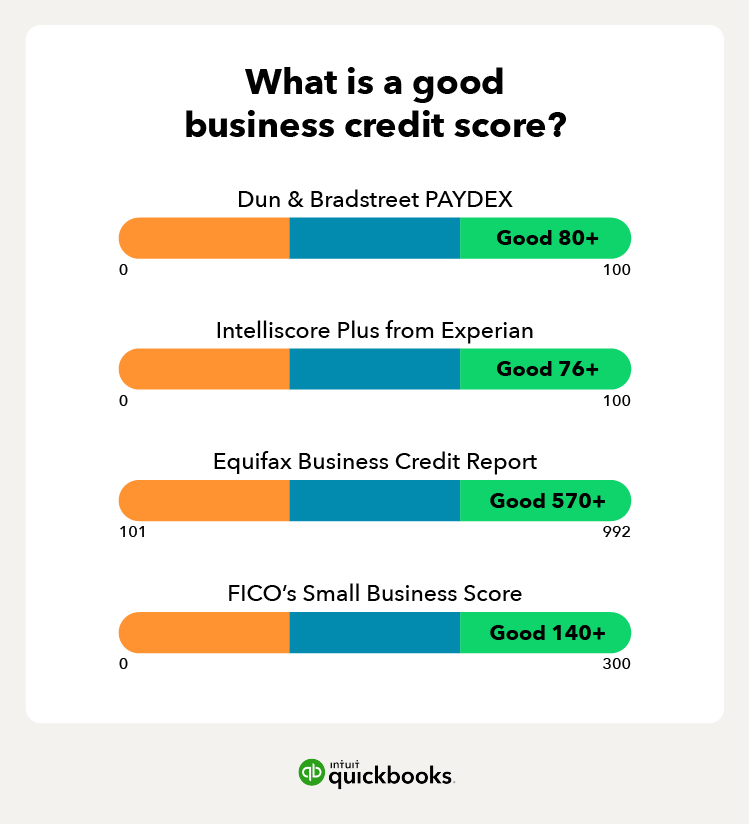

What credit score is needed for a business line of credit?

The credit score required for a business line of credit can vary depending on the lender and the specific terms of the loan. Typically, a good credit score is considered to be 700 or higher, but some lenders may accept lower credit scores if the business has a strong financial history and a solid business plan.

Understanding Business Credit Scores

To determine the credit score needed for a business line of credit, it’s essential to understand how business credit scores work. A business credit score is a numerical representation of a company’s creditworthiness, taking into account its payment history, credit utilization, and other factors. The credit score range for businesses is typically between 300 and 850, with higher scores indicating a lower credit risk. Some key factors that can affect a business credit score include:

- Payment history: A history of on-time payments can help improve a business’s credit score.

- Credit utilization: Keeping credit utilization rates low can also contribute to a higher credit score.

- Credit age: A longer credit history can be beneficial for a business’s credit score.

Factors That Affect Business Line of Credit Approval

When applying for a business line of credit, lenders consider various factors beyond just the credit score. These factors can include the business’s annual revenue, cash flow, and industry. A business with a strong financial history and a solid business plan may be more likely to qualify for a business line of credit, even with a lower credit score. Some key factors that can affect business line of credit approval include:

- Revenue growth: A business with a history of revenue growth may be more attractive to lenders.

- Cash flow management: A business with strong cash flow management can demonstrate its ability to repay loans.

- Industry risk: Businesses in high-risk industries may face stricter lending requirements.

Alternatives to Traditional Business Lines of Credit

For businesses with poor credit or limited credit history, there may be alternative options to traditional business lines of credit. These can include invoice financing, equipment financing, and online lenders that offer more flexible credit requirements. Some benefits of these alternative options include:

- Easier approval: Alternative lenders may have more lenient credit requirements.

- Faster funding: Alternative lenders can often provide faster funding than traditional lenders.

- More flexible terms: Alternative lenders may offer more flexible repayment terms and interest rates.

What is the fastest way to get business credit for an LLC?

The fastest way to get business credit for an LLC is to establish a strong credit profile and follow a strategic approach to building credit. This involves obtaining an Employer Identification Number (EIN), opening a business bank account, and applying for credit cards or loans in the company’s name. By doing so, the LLC can start building a credit history and increase its chances of getting approved for credit lines or loans in the future.

Establishing a Business Credit Profile

To establish a business credit profile, the LLC must take several steps, including:

- Obtaining an EIN from the Internal Revenue Service (IRS), which is a unique identifier for the business

- Registering the business with the Secretary of State and obtaining any necessary licenses and permits

- Opening a business bank account in the company’s name, which will help to separate personal and business finances

This will help to create a separate credit identity for the business, which is essential for building business credit.

Building Business Credit through Credit Cards and Loans

Building business credit through credit cards and loans involves applying for credit in the company’s name and making on-time payments. This can be done by:

- Applying for a business credit card, which can be used to make purchases and pay for expenses

- Taking out a small loan or line of credit, which can be used to finance business operations or expansion

- Making regular payments on the credit card or loan, which will help to build a positive credit history

By doing so, the LLC can establish a strong credit history and increase its credit score, making it easier to get approved for credit in the future.

Maintaining and Monitoring Business Credit

Maintaining and monitoring business credit involves regularly checking the company’s credit report and credit score, and making adjustments as needed. This can be done by:

- Checking the business credit report regularly to ensure it is accurate and up-to-date

- Monitoring the credit score and making adjustments to improve it, such as paying off debt or reducing credit utilization

- Updating the credit profile as needed, such as adding new credit accounts or removing old ones

By maintaining and monitoring business credit, the LLC can ensure that its credit profile is strong and accurate, which can help to increase its chances of getting approved for credit and loans in the future, with low interest rates and favorable terms.

Can a new LLC get a business line of credit?

A new LLC can get a business line of credit, but it may be more challenging than for established businesses. Lenders typically consider the creditworthiness of the business and its owners when evaluating a line of credit application. Since a new LLC has no established credit history, lenders may require the owners to provide a personal guarantee or collateral to secure the line of credit.

Eligibility Requirements for a New LLC

To qualify for a business line of credit, a new LLC must meet certain eligibility requirements. The business must have a valid business license and a Employer Identification Number (EIN). The owners must also provide personal and business financial statements, including tax returns and bank statements. Some lenders may also require a business plan and projection of future income. Here are some key requirements:

- The LLC must have a minimum credit score of 600, although some lenders may require a higher score.

- The business must have a stable cash flow and a positive net income.

- The owners must have a good personal credit history and a low debt-to-income ratio.

Options for New LLCs to Get a Business Line of Credit

New LLCs have several options to get a business line of credit. They can apply for a line of credit from a traditional bank or alternative lender. Some lenders specialize in providing lines of credit to new businesses and may have more flexible requirements. New LLCs can also consider online lenders that offer fast and easy applications. Here are some options:

- Traditional banks: Offer low interest rates and long repayment terms, but may have stricter requirements.

- Alternative lenders: Provide faster funding and more flexible requirements, but may have higher interest rates.

- Online lenders: Offer easy applications and fast funding, but may have higher fees and shorter repayment terms.

Benefits of a Business Line of Credit for a New LLC

A business line of credit can provide several benefits for a new LLC. It can help the business manage cash flow and cover unexpected expenses. A line of credit can also provide flexibility and convenience, allowing the business to borrow and repay funds as needed. Here are some benefits:

- Improved cash flow: A line of credit can help the business cover gaps in cash flow and avoid late payments.

- Increased flexibility: A line of credit provides access to funds when needed, allowing the business to take advantage of opportunities.

- Better financial management: A line of credit can help the business manage expenses and make strategic investments.

Frequently Asked Questions

What is Commercial Financing and How Can it Help My Business?

Commercial financing refers to the process of obtaining funding for your business through various lending institutions, such as banks, credit unions, or alternative lenders. This type of financing can provide your business with the necessary capital to invest in new projects, expand your operations, or simply to cover day-to-day expenses. With commercial financing, you can access loans, lines of credit, or other financial products that cater to your specific business needs. By leveraging commercial financing, you can grow your business, increase revenue, and stay competitive in the market. It’s essential to understand the different types of commercial financing options available, such as term loans, invoice financing, and equipment financing, to determine which one best suits your business requirements.

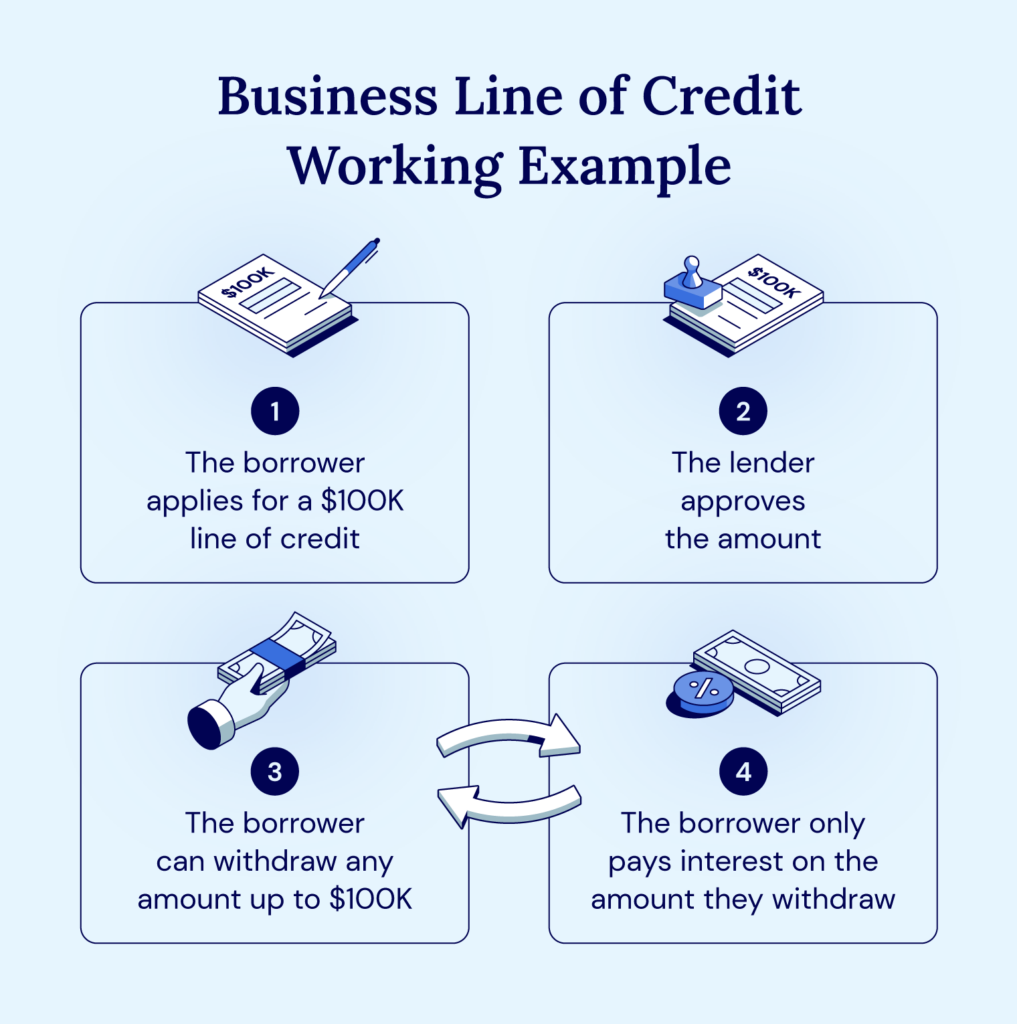

How Do Business Credit Lines Work and What Are the Benefits?

A business credit line is a type of revolving credit that allows you to access funds as needed, up to a predetermined credit limit. This financial product provides your business with flexibility and convenience, enabling you to draw upon the credit line at any time to cover unexpected expenses or to take advantage of new business opportunities. The benefits of a business credit line include easy access to capital, competitive interest rates, and the ability to repay and re-borrow funds as needed. By having a business credit line in place, you can manage cash flow more effectively, smooth out fluctuations in revenue, and make strategic investments in your business. Additionally, a business credit line can help you build credit and establish a positive credit history, which can be beneficial for future borrowing needs.

What Are the Key Differences Between Commercial Financing and Traditional Bank Loans?

Commercial financing and traditional bank loans differ in several key ways, including approval rates, loan terms, and interest rates. Commercial financing options, such as alternative lending, often have more relaxed criteria for approval, which can make it easier for businesses with poor credit or limited history to access funding. In contrast, traditional bank loans typically require strong credit and a stable financial history, which can make it more challenging for some businesses to qualify. Additionally, commercial financing options may offer more flexible repayment terms and competitive interest rates compared to traditional bank loans. Understanding the pros and cons of each option is crucial to determining which one is best suited to your business needs and goals. By considering factors such as loan amounts, fees, and repayment schedules, you can make an informed decision about which type of financing is right for your business.

How Can I Determine Which Commercial Financing Option is Best for My Business?

Determining the best commercial financing option for your business requires a thorough evaluation of your financial situation, business goals, and industry. It’s essential to assess your business’s creditworthiness, cash flow, and collateral to determine which financing options are available to you. You should also consider factors such as interest rates, fees, and repayment terms when evaluating different commercial financing options. Additionally, it’s crucial to research and compare different lenders and financial products to find the one that best meets your business needs. By consulting with a financial advisor or lending expert, you can gain a deeper understanding of the commercial financing landscape and make an informed decision about which option is right for your business. Ultimately, the best commercial financing option will depend on your business’s unique circumstances and goals, so it’s essential to take the time to carefully evaluate your options and choose the one that aligns with your business strategy.