Starting a small business can be a thrilling venture, but it often requires a significant amount of capital to get off the ground. Traditional lending options can be inflexible and time-consuming, leaving entrepreneurs in a difficult spot. Fortunately, small business loans offer a fast and flexible financing solution, providing the necessary funds to turn a business idea into a reality. With a range of options available, entrepreneurs can secure the funding they need to grow and succeed, making their business dreams a tangible reality in a relatively short period of time with minimal hassle.

Introduction to Small Business Loans Getting a small business loan can be a great way to finance your business and help it grow. There are many different types of loans available, and the right one for you will depend on your business needs and credit score. In this guide, we will explore the different types of small business loans and how to get fast and flexible financing.

What are Small Business Loans?

Small business loans are a type of funding that allows business owners to borrow money to finance their business. These loans can be used for a variety of purposes, such as expanding your business, hiring new employees, or purchasing new equipment. There are many different types of small business loans available, including term loans, lines of credit, and invoice financing.

Types of Small Business Loans

There are many different types of small business loans available, each with its own benefits and drawbacks. Some of the most common types of small business loans include:

| Loan Type | Description |

|---|---|

| Term Loan | A fixed-rate loan that is paid back over a set period of time |

| Line of Credit | A revolving line of credit that allows you to borrow and repay funds as needed |

| Invoice Financing | A type of loan that allows you to borrow money based on outstanding invoices |

These loans can be used for a variety of purposes, and the right one for you will depend on your business needs and financial situation.

How to Get a Small Business Loan

Getting a small business loan can be a challenging process, but there are several steps you can take to improve your chances of getting approved. These include: Checking your credit score to make sure it is good enough to qualify for a loan Preparing a strong business plan that outlines your business goals and financial projections Shopping around for different loan options to find the best rates and terms Providing collateral to secure the loan and reduce the risk of default

Beware of Small Business Loan Scams

There are many scams and predatory lenders that target small business owners, so it’s essential to be cautious when applying for a loan. Some red flags to watch out for include: High interest rates or hidden fees Unclear terms or conditions Pressure to sign a loan agreement quickly Unlicensed lenders or unregistered loan brokers It’s essential to do your research and due diligence before applying for a loan to avoid falling victim to a scam.

Small Business Loan Alternatives

If you’re having trouble getting approved for a small business loan, there are several alternatives you can consider. These include: Crowdfunding platforms that allow you to raise money from a large number of people Grants and subsidies that provide free money to small businesses Invoice financing and factoring that allow you to borrow money based on outstanding invoices Community development financial institutions that provide alternative loan options to small businesses These alternatives can provide fast and flexible financing options for small businesses that may not qualify for traditional loans.

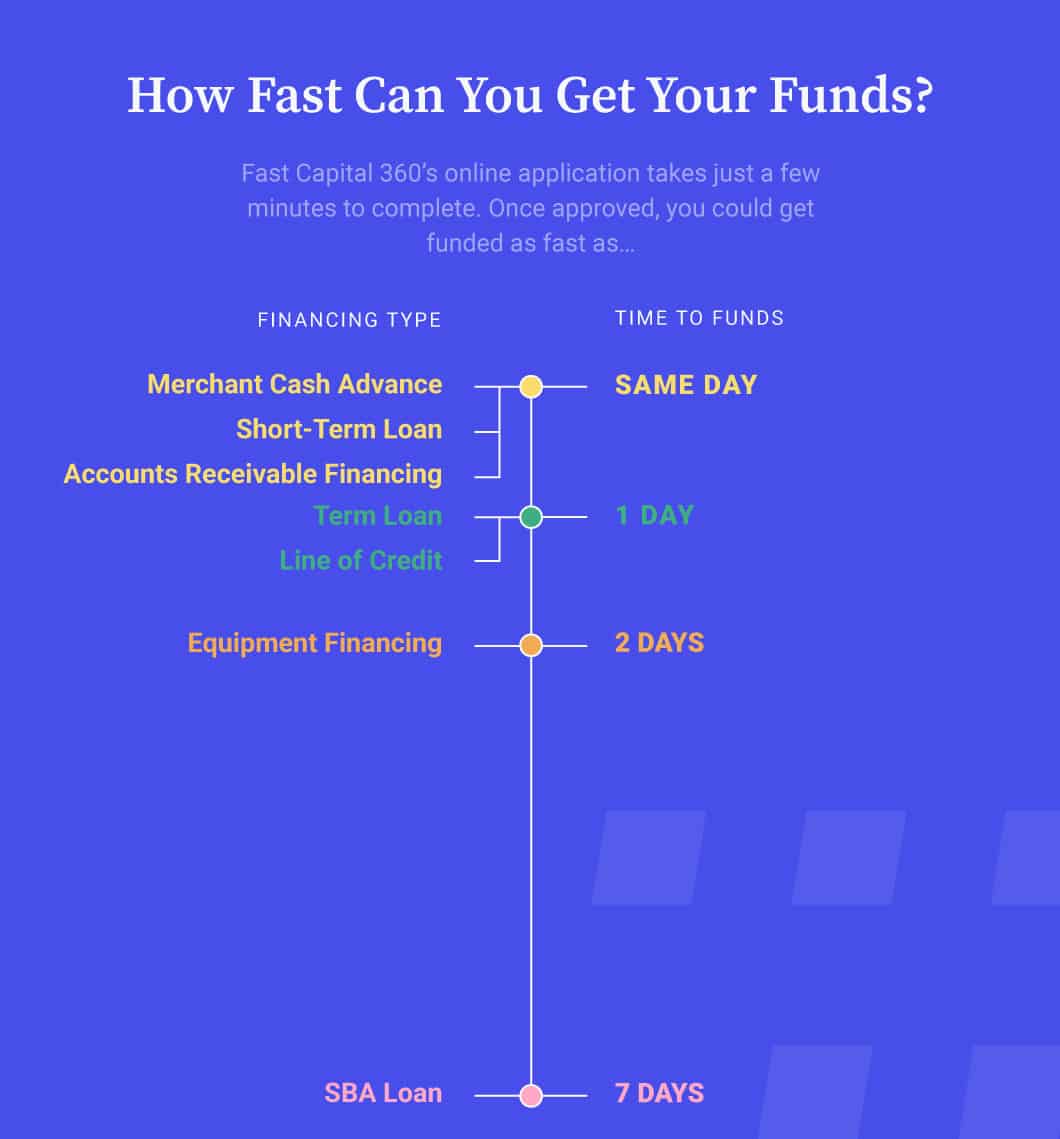

How fast can you get a small business loan?

Getting a small business loan can be a relatively quick process, depending on the lender and the borrower’s qualifications. The lending process typically involves an application, review, and approval, which can take anywhere from a few hours to several weeks. Online lenders have streamlined the process, offering fast funding options with minimal paperwork and quick decisions.

Types of Small Business Loans

There are various types of small business loans, each with its own funding speed. Some popular options include short-term loans, line of credit, and invoice financing. These loans cater to different business needs, such as cash flow management or equipment financing. Here are some key features of these loan types:

- Short-term loans: Provide quick access to funds, usually with a repayment term of less than a year.

- Line of credit: Offers flexible funding, allowing businesses to borrow and repay funds as needed.

- Invoice financing: Enables businesses to unlock cash tied up in outstanding invoices, improving cash flow.

Factors Affecting Loan Approval Speed

Several factors can influence the speed of loan approval, including the borrower’s credit score, business financials, and industry type. Lenders may also consider the loan amount, repayment term, and collateral when making a decision. A strong business plan and financial statements can help demonstrate the borrower’s creditworthiness and repayment ability. Here are some key factors to consider:

- Credit score: A good credit score can help businesses qualify for better loan terms and faster funding.

- Business financials: Lenders review financial statements, such as balance sheets and income statements, to assess the business’s financial health.

- Industry type: Certain industries, such as retail or food service, may be considered higher risk and require more extensive underwriting.

Ways to Expedite the Loan Process

Businesses can take several steps to expedite the loan process, including preparing a solid application package and working with a lender that offers streamlined underwriting. Additionally, having a clear understanding of the business’s financial needs and goals can help borrowers navigate the lending process more efficiently. Here are some tips to help businesses speed up the loan process:

- Gather required documents: Ensure all necessary documents, such as tax returns and bank statements, are readily available.

- Choose a lender with a simple application process: Look for lenders that offer online applications and minimal paperwork.

- Be prepared to provide additional information: Lenders may request supplemental documentation or explanations to support the loan application.

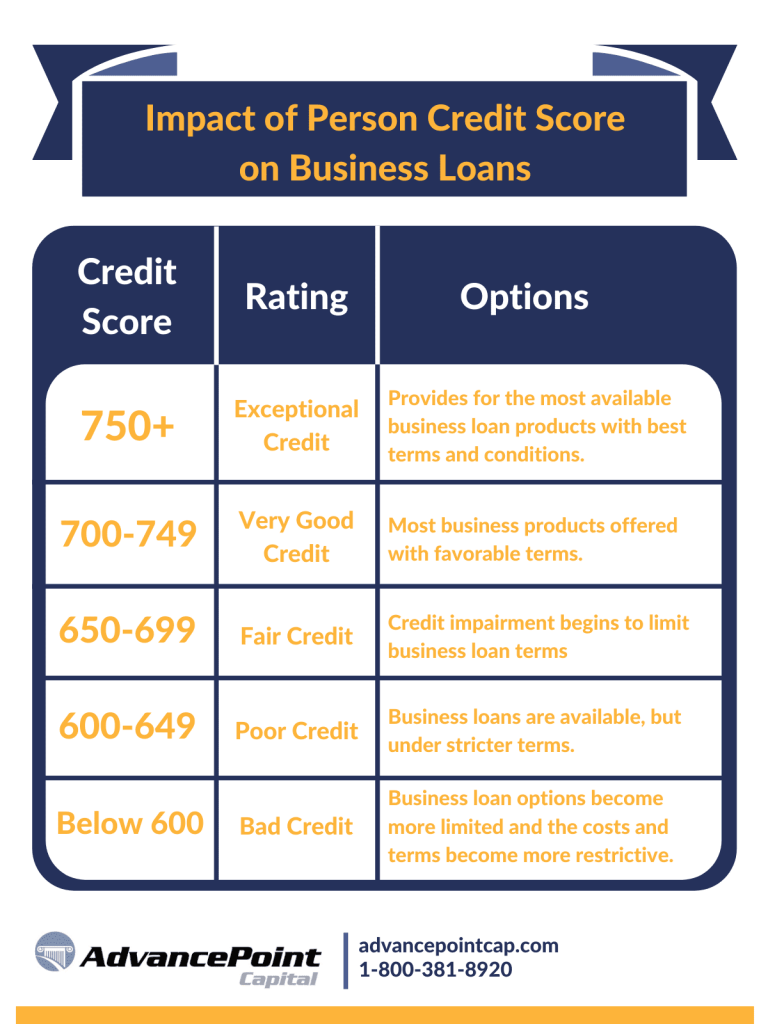

What is the minimum credit score to get a small business loan?

The minimum credit score to get a small business loan varies depending on the lender and the type of loan. However, most lenders require a credit score of at least 600 to consider a small business loan application. Some lenders may have more stringent requirements, while others may be more lenient. It’s essential for small business owners to understand that their personal credit score can impact their ability to secure a loan for their business.

Understanding Credit Score Requirements

The credit score requirements for small business loans can vary depending on the lender and the type of loan. For example, a bank loan may require a higher credit score than an alternative lender. Here are some general guidelines:

- A credit score of 650 or higher is generally considered good and may qualify for a lower interest rate.

- A credit score between 600 and 649 may qualify for a loan, but with a higher interest rate.

- A credit score below 600 may make it difficult to qualify for a loan, but some lenders may still consider the application.

Factors That Affect Credit Score

Several factors can affect a small business owner’s credit score, including their payment history, credit utilization, and credit age. Here are some key factors to consider:

- Payment history accounts for 35% of the credit score, so making on-time payments is essential.

- Credit utilization accounts for 30% of the credit score, so keeping credit card balances low is crucial.

- Credit age accounts for 15% of the credit score, so a longer credit history can be beneficial.

Improving Credit Score for Small Business Loan

Small business owners can take steps to improve their credit score and increase their chances of securing a loan. Here are some strategies:

- Monitor credit reports regularly to ensure accuracy and dispute any errors.

- Make on-time payments to demonstrate a positive payment history.

- Keep credit card balances low to maintain a healthy credit utilization ratio.

What disqualifies you from getting an SBA loan?

Several factors can disqualify you from obtaining a loan from the Small Business Administration (SBA). The SBA has strict requirements for loan applicants, and failing to meet these requirements can result in loan denial. Some of the key factors that can disqualify you from getting an SBA loan include poor credit history, inadequate collateral, and insufficient business experience.

Eligibility Requirements

To qualify for an SBA loan, your business must meet certain eligibility requirements. These requirements include being a for-profit business, having a physical location in the United States, and being small as defined by the SBA. Additionally, your business must be owner-operated, and you must have invested your own time and money in the business. Some of the key eligibility requirements include:

- Being a citizen or permanent resident of the United States

- HAVING a good credit history with a minimum credit score of 620

- Having a solid business plan and projections for future growth

Funding Options and Limitations

The SBA offers several funding options, including the 7(a) loan program, the Microloan program, and the CDC/504 loan program. However, each of these programs has its own limitations and restrictions. For example, the 7(a) loan program has a maximum loan amount of $5 million, while the Microloan program has a maximum loan amount of $50,000. Some of the key limitations and restrictions include:

- Loan amounts and interest rates that may not be competitive with other lenders

- Collateral requirements that may be difficult to meet for some businesses

- Restrictions on use of funds that may limit your ability to use the loan for certain purposes

Creditworthiness and Risk Assessment

The SBA uses a creditworthiness and risk assessment framework to evaluate loan applicants. This framework includes an evaluation of your credit history, business experience, and financial situation. The SBA also considers industry trends and market conditions when evaluating loan applications. Some of the key factors that are considered in the creditworthiness and risk assessment include:

- Payment history and credit score to determine your creditworthiness

- Business experience and management team to determine your ability to repay the loan

- Financial statements and projections to determine your financial situation and potential for growth

Frequently Asked Questions

What are small business loans and how do they work?

Small business loans are a type of financing designed to help entrepreneurs and small business owners access the capital they need to launch, grow, or expand their businesses. These loans can be used for a variety of purposes, such as purchasing equipment, hiring staff, marketing, or covering operational costs. The application process typically involves submitting a business plan, financial statements, and other documentation to a lender, who will then review the application and determine the loan amount, interest rate, and repayment terms. Flexible financing options are available, including short-term loans, long-term loans, and lines of credit, to help business owners manage their cash flow and achieve their goals.

What are the benefits of getting a small business loan?

There are several benefits to getting a small business loan, including fast access to capital, flexible repayment terms, and the ability to separate personal and business finances. A small business loan can provide the funding needed to invest in growth opportunities, such as hiring new staff, expanding into new markets, or developing new products. Additionally, a small business loan can help business owners manage cash flow and cover unexpected expenses, such as equipment repairs or unforeseen expenses. Interest rates on small business loans can be competitive, and lenders may offer special programs or incentives to help small businesses thrive. By getting a small business loan, entrepreneurs can focus on growing their business, rather than worrying about financing.

How do I qualify for a small business loan?

To qualify for a small business loan, applicants typically need to meet certain eligibility criteria, such as having a established business, a good credit history, and a solid business plan. Lenders will also consider the business’s financial health, including revenue, profitability, and cash flow, as well as the owner’s personal credit score and experience. Some lenders may require collateral, such as equipment or property, to secure the loan, while others may offer unsecured loans. Alternative lenders may have more flexible qualification requirements, and may consider non-traditional credit data, such as social media or online reviews, when making a lending decision. It’s essential to review the lender’s requirements and prepare a strong application to increase the chances of approval.

How can I apply for a small business loan and what documents do I need?

To apply for a small business loan, applicants can typically submit an online application or visit a lender’s website to initiate the process. The application will require basic business information, such as the business name, address, and tax ID number, as well as financial data, including income statements, balance sheets, and cash flow statements. Lenders may also require additional documents, such as a business plan, resumes of key management, and industry reports, to help assess the business’s creditworthiness. Applicants should be prepared to provide detailed information about their business, including growth plans, marketing strategies, and financial projections, to demonstrate their creditworthiness and increase their chances of securing a loan. Lenders may offer streamlined applications or digital platforms to make the application process more efficient and convenient.