Acquiring the right equipment is crucial for businesses to stay competitive and efficient. Investing in new machinery and technology can be expensive, making it challenging for companies to allocate funds. Equipment loans offer a solution, providing financing options to purchase or lease necessary equipment, helping businesses to upgrade and expand their operations without depleting cash reserves. With flexible repayment terms and various loan options available, companies can now acquire the equipment they need to drive growth and success, making equipment loans an attractive financing solution for businesses of all sizes and industries. This financing option helps companies thrive.

Introduction to Equipment Loans

Equipment loans are a type of financing that allows businesses to acquire the machinery and technology they need to operate and grow. These loans are specifically designed to help companies purchase or lease equipment, such as computers, software, vehicles, and production machinery. By financing equipment, businesses can conserve their cash flow and allocate their resources more efficiently.

Benefits of Equipment Loans

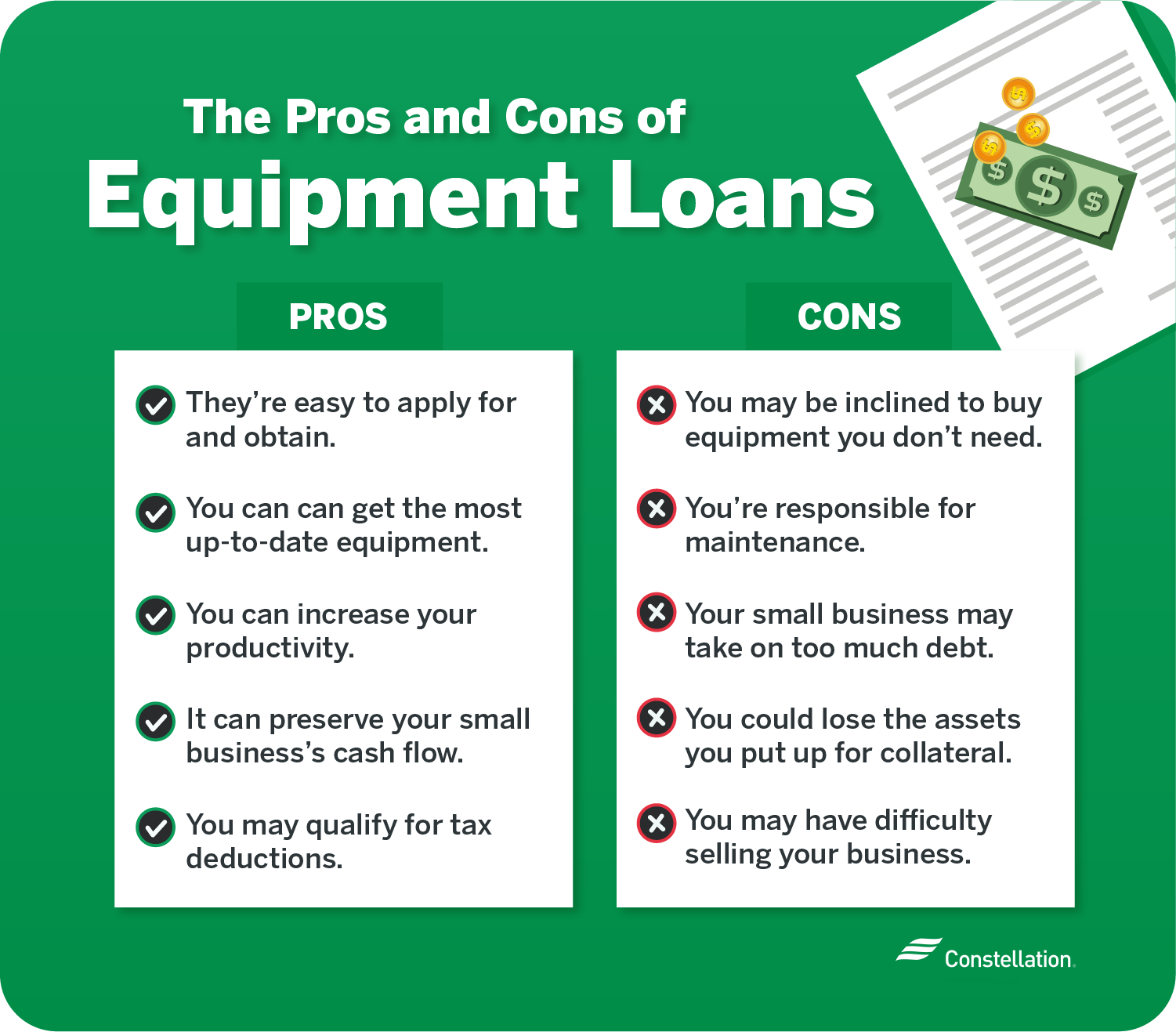

The benefits of equipment loans are numerous. For one, they enable businesses to acquire state-of-the-art equipment without having to pay the full purchase price upfront. This can help companies stay competitive and improve their productivity. Additionally, equipment loans can provide tax benefits, such as depreciation deductions, which can help reduce a company’s tax liability. Some equipment loans also offer flexible repayment terms, which can help businesses manage their cash flow more effectively.

Types of Equipment Loans

There are several types of equipment loans available, including:

| Loan Type | Description |

|---|---|

| Term Loan | A loan with a fixed interest rate and repayment term |

| Line of Credit | A revolving credit line that allows businesses to borrow and repay funds as needed |

| Lease Financing | A loan that allows businesses to lease equipment for a fixed period of time |

Each type of equipment loan has its own advantages and disadvantages, and the right choice will depend on the specific needs and financial situation of the business.

How to Qualify for an Equipment Loan

To qualify for an equipment loan, businesses typically need to meet certain creditworthiness and financial stability requirements. This may include having a good credit score, a stable cash flow, and a solid business plan. The lender will also want to know the purpose of the loan and the type of equipment being financed. Additionally, the lender may require collateral, such as the equipment being financed, to secure the loan.

Best Practices for Equipment Loan Management

To get the most out of an equipment loan, businesses should follow some best practices, such as: Carefully reviewing and understanding the loan terms and conditions Tracking and managing the loan payments and interest rates Maintaining and upgrading the equipment to ensure it remains operative and efficient Monitoring the cash flow and financial performance to ensure the loan is not negatively impacting the business By following these best practices, businesses can ensure that their equipment loan is a valuable investment that supports their growth and success.

What is an example of an equipment loan?

An example of an equipment loan is when a company borrows a piece of equipment, such as a crane or a forklift, from a lender for a specific period of time in exchange for periodic payments. This type of loan allows businesses to use the equipment they need without having to pay the full purchase price upfront. The lender retains ownership of the equipment until the loan is fully repaid, and the borrower is responsible for maintenance and insurance costs.

Types of Equipment Loans

Equipment loans can be used for a variety of purposes, including construction, manufacturing, and agriculture. Some common examples of equipment loans include loans for vehicles, machinery, and technology. The terms of an equipment loan can vary depending on the lender and the type of equipment being borrowed. Here are some key features of equipment loans:

- The loan period can range from a few months to several years, depending on the type of equipment and the borrower’s needs.

- The interest rate on an equipment loan can be fixed or variable, and may be influenced by the borrower’s credit score and the value of the equipment.

- The loan may require a down payment, which can be a percentage of the equipment’s purchase price.

Benefits of Equipment Loans

Equipment loans can offer several benefits to businesses, including increased cash flow and improved efficiency. By borrowing equipment rather than purchasing it outright, companies can conserve their capital and allocate it to other areas of the business. Additionally, equipment loans can provide businesses with access to new technology and specialized equipment that they might not be able to afford otherwise. Here are some of the advantages of equipment loans:

- Flexibility: Equipment loans can be structured to meet the specific needs of the borrower, with options for different loan terms and repayment schedules.

- Tax benefits: The interest payments on an equipment loan may be tax-deductible, which can help reduce the borrower’s taxable income.

- Upgrading equipment: Equipment loans can provide businesses with the opportunity to upgrade their equipment and stay competitive in their industry.

Risks and Considerations

While equipment loans can be a useful financing option for businesses, there are also some risks and considerations to be aware of. For example, the borrower may be responsible for maintenance and repair costs, which can add to the overall cost of the loan. Additionally, the borrower may be required to provide collateral to secure the loan, which can put their assets at risk if they default on the loan. Here are some potential risks and considerations:

- Default risk: If the borrower is unable to make the loan payments, they may face penalties and fees, and may even lose the equipment or other assets.

- Obsolescence: The equipment being borrowed may become outdated or obsolete during the loan period, which can affect its value and the borrower’s ability to use it.

- Insurance requirements: The borrower may be required to purchase insurance to cover the equipment against damage or loss, which can add to the overall cost of the loan.

What credit score do you need for an equipment loan?

To qualify for an equipment loan, you typically need a good credit score, which can vary depending on the lender and the type of equipment being financed. Generally, a credit score of 600 or higher is considered good, but some lenders may require a minimum credit score of 650 or 700. It’s essential to check with the lender for their specific credit score requirements.

Understanding Credit Score Requirements for Equipment Loans

The credit score required for an equipment loan depends on various factors, including the lender, the type of equipment, and the loan amount. A higher credit score can help you qualify for better interest rates and loan terms. Here are some key factors to consider:

- The lender’s credit score requirements can vary, so it’s crucial to shop around and compare rates and terms from different lenders.

- A good credit history can help you qualify for an equipment loan with a lower interest rate and more favorable terms.

- Some lenders may offer equipment loans with bad credit, but these loans often come with higher interest rates and stricter terms.

How Credit Scores Affect Equipment Loan Interest Rates

Your credit score can significantly impact the interest rate you qualify for on an equipment loan. A higher credit score can help you qualify for a lower interest rate, which can save you money over the life of the loan. Here are some ways your credit score can affect your interest rate:

- A good credit score can help you qualify for a lower interest rate, which can reduce your monthly payments and save you money over time.

- A poor credit score can result in a higher interest rate, which can increase your monthly payments and cost you more in interest over the life of the loan.

- Some lenders may offer interest rate discounts for borrowers with excellent credit, which can help you save even more money on your equipment loan.

Improving Your Credit Score to Qualify for an Equipment Loan

If you have a poor credit score, there are steps you can take to improve your credit and qualify for an equipment loan. Here are some tips to help you boost your credit score:

- Make on-time payments on your credit accounts to demonstrate your creditworthiness and responsibility.

- Reduce your debt by paying down outstanding balances and avoiding new credit inquiries.

- Monitor your credit report for errors and dispute any inaccuracies to ensure your credit score is accurate and reflects your credit history.

What are equipment financing loans?

Equipment financing loans are a type of loan that allows businesses to purchase or lease equipment and machinery necessary for their operations. These loans are designed to help companies acquire the assets they need to run their business efficiently, without having to pay the full cost upfront. The equipment serves as collateral for the loan, which means that the lender can seize the equipment if the borrower defaults on the loan.

Types of Equipment Financing Loans

Equipment financing loans can be categorized into different types, depending on the equipment being financed and the terms of the loan. Some common types of equipment financing loans include:

- Term Loans: These loans have a fixed interest rate and a specified repayment term, which can range from a few months to several years.

- Lines of Credit: These loans provide businesses with a revolving credit line that can be used to purchase equipment and other business assets.

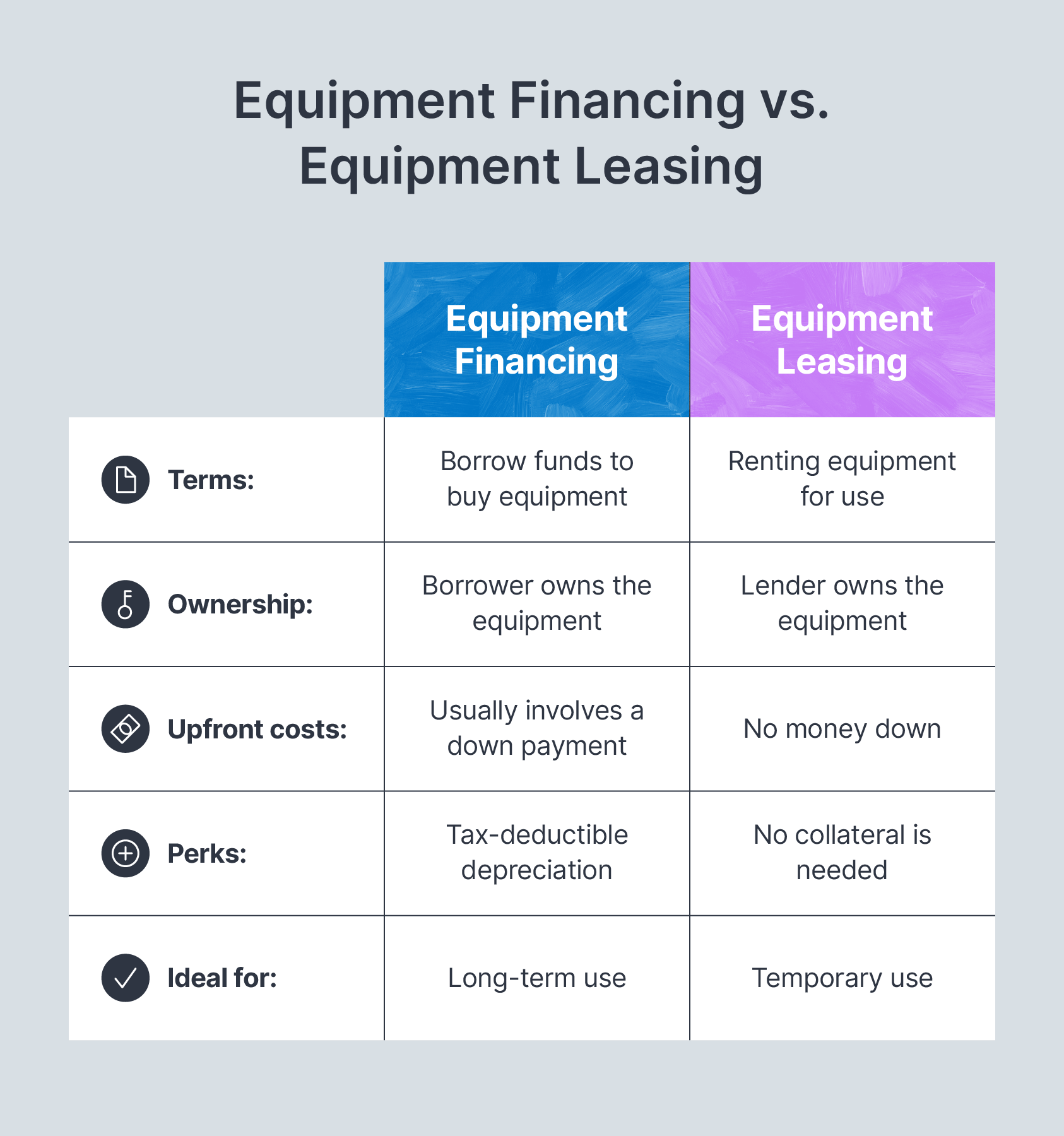

- Lease Financing: This type of loan allows businesses to lease equipment for a specified period, rather than purchasing it outright.

Benefits of Equipment Financing Loans

Equipment financing loans offer several benefits to businesses, including the ability to conserve cash and preserve credit. By financing equipment purchases, businesses can avoid tying up large amounts of cash in a single asset. Additionally, equipment financing loans can help businesses to:

- Improve Cash Flow: By spreading the cost of equipment over several months or years, businesses can better manage their cash flow and avoid large upfront payments.

- Increase Efficiency: By acquiring the equipment they need, businesses can increase productivity and efficiency, which can lead to increased revenue and profitability.

- Stay Competitive: Equipment financing loans can help businesses to stay competitive by allowing them to acquire the latest technology and equipment, which can give them an edge over their competitors.

How to Qualify for Equipment Financing Loans

To qualify for equipment financing loans, businesses typically need to meet certain eligibility criteria, including a good credit history and a stable financial situation. Lenders will also consider the type and value of the equipment being financed, as well as the business’s ability to repay the loan. Some key factors that lenders consider when evaluating loan applications include:

- Credit Score: A good credit score can help businesses to qualify for better interest rates and terms.

- Business History: A stable business history and a strong track record of repaying debts can help businesses to qualify for equipment financing loans.

- Equipment Value: The value of the equipment being financed will also be considered, as well as its useful life and resale value.

Who has the best equipment financing?

To determine who has the best equipment financing, it’s essential to consider various factors, including interest rates, repayment terms, and lender requirements. Different lenders offer distinct financing options, and the best one for a particular business depends on its specific needs and circumstances. Some lenders specialize in financing specific types of equipment, while others provide more general financing options.

Types of Equipment Financing

The type of equipment financing a business chooses can significantly impact its operations and financial stability. Some common types of equipment financing include leases, loans, and lines of credit. Each option has its advantages and disadvantages, and businesses must carefully consider their needs and financial situation before making a decision. Here are some key points to consider:

- Leases can provide businesses with access to equipment without requiring a significant upfront investment.

- Loans can offer more flexibility in terms of repayment terms and interest rates.

- Lines of credit can provide businesses with a flexible source of funding for equipment purchases and other business needs.

Top Equipment Financing Providers

Several lenders offer equipment financing options, and the best provider for a particular business depends on its specific needs and circumstances. Some top equipment financing providers include CIT, Wells Fargo, and Bank of America. These lenders offer a range of financing options, including leases, loans, and lines of credit. Here are some key points to consider:

- CIT offers a range of equipment financing options, including leases and loans, with competitive interest rates and flexible repayment terms.

- Wells Fargo provides equipment financing options, including leases and loans, with variable interest rates and repayment terms.

- Bank of America offers equipment financing options, including leases and loans, with fixed interest rates and repayment terms.

Benefits of Equipment Financing

Equipment financing can provide businesses with several benefits, including increased cash flow, improved efficiency, and enhanced competitiveness. By financing equipment purchases, businesses can conserve capital and allocate it to other business needs, such as hiring employees or expanding operations. Here are some key points to consider:

- Equipment financing can help businesses conserve capital and allocate it to other business needs.

- Equipment financing can improve efficiency by providing businesses with access to new and improved equipment.

- Equipment financing can enhance competitiveness by enabling businesses to invest in new technologies and processes.

Frequently Asked Questions

What are equipment loans and how do they work for businesses?

Equipment loans are a type of financing that allows businesses to acquire and utilize necessary machinery and technology to operate and grow. These loans provide companies with the funds needed to purchase or lease equipment, such as computers, software, manufacturing equipment, and other essential tools. The loan is typically secured by the equipment itself, meaning that the lender can repossess the equipment if the business defaults on the loan. With equipment loans, businesses can finance up to 100% of the equipment’s purchase price, and repayment terms can range from a few months to several years, depending on the lender and the type of equipment being financed. This type of financing is especially useful for small businesses or startups that may not have the necessary capital to purchase equipment outright.

What types of equipment can be financed with an equipment loan?

Equipment loans can be used to finance a wide range of machinery and technology, including construction equipment, agricultural equipment, medical equipment, and office equipment. Additionally, loans can be used to finance software, hardware, and other technology solutions, such as computer systems, telecommunications equipment, and networking infrastructure. Some lenders may also offer specialized financing options for specific types of equipment, such as energy-efficient equipment or sustainable technology solutions. The key is to find a lender that understands the specific needs of your business and can provide flexible financing options that align with your business goals. By financing the right equipment, businesses can increase efficiency, reduce costs, and improve productivity, ultimately leading to growth and success.

What are the benefits of using an equipment loan to finance business equipment?

There are several benefits to using an equipment loan to finance business equipment, including preserving cash flow, reducing upfront costs, and improving credit scores. By financing equipment through a loan, businesses can conserve their working capital and use it for other essential expenses, such as payroll, rent, and marketing. Additionally, equipment loans can provide tax benefits, as the interest paid on the loan may be tax-deductible. Furthermore, equipment loans can help businesses stay up-to-date with the latest technology and machinery, which can improve efficiency, increase productivity, and enhance competitiveness. By using an equipment loan, businesses can also avoid obsolescence and repair costs associated with outdated equipment, ultimately leading to long-term savings and growth.

How do I qualify for an equipment loan, and what are the typical requirements?

To qualify for an equipment loan, businesses typically need to meet certain credit and financial requirements, such as a good credit score, stable cash flow, and a solid business plan. Lenders may also require collateral, such as the equipment being financed, to secure the loan. The application process typically involves submitting financial statements, tax returns, and other documentation to demonstrate the business’s creditworthiness and ability to repay the loan. Some lenders may also require a down payment or equity in the business. The interest rate and repayment terms of the loan will depend on the lender, the type of equipment being financed, and the business’s credit profile. It’s essential to shop around and compare different lenders and loan options to find the best fit for your business needs and goals, and to ensure that you understand all the terms and conditions of the loan before signing.